Financing

Those in favor of legalization presume that the level of insider trading would remain relatively low, even after being permitted, because such trades would be limited by the personal wealth of the individual insiders (Dent 252). Essentially, individuals could only invest as much money as they had, which would limit returns and thus limit the use of IT. However, one must consider that insiders could easily obtain financing to exploit an informational advantage (Dent 252). If insider trading were legal, insiders would be free to seek outside financing for trading. Insiders could borrow money for stock trading “on margin,” similarly to how outsiders do today (Dent 252). By having inside information and an almost guarantee of beating the market, they would be able to borrow more money than outsider investors. Lenders would have greater incentive to lend money to an insider rather than an outsider. Inside traders are less risky because returns are practically guaranteed. Due to this guarantee, insiders could also use more personal assets like their homes to secure loans that a prudent outsider would not or could not. This increased borrowing could multiply the trading capacity of insiders (Dent 252). Insiders could also sell their information. This would allow the wealthy to reap greater profits because they have greater capital to stake (Dent 252). Many question the fairness of widespread insider trading and the numerous unknown effects.

The 1920’s Argument

Some proponents defend against claims that IT will deter outside investment in the way that opponents speculate by making reference to the 1920’s stock market. Proponents say that insider trading was not clearly illegal in the 1920’s, yet did not deter outside trading (Dent 260). However, the stock market is different than it was in the 20’s. Most traders were individuals with little knowledge of risk. Nowadays, experienced firms and institutions do most of the trading. Also, no other foreign markets had barred insider trading yet, so there were not better alternatives than the U.S., markets in the 1920’s (Dent 260). If the U.S. legalized insider trading today, investors have the opportunity to simply invest in foreign markets instead. One should also note that the various conditions of the 1920’s market contributed to the Crash of 1929. Those who use this reference to historical conditions simply not consider the complexities of today’s markets. This paper will argue that IT could deter investments.

Those in favor of legalization presume that the level of insider trading would remain relatively low, even after being permitted, because such trades would be limited by the personal wealth of the individual insiders (Dent 252). Essentially, individuals could only invest as much money as they had, which would limit returns and thus limit the use of IT. However, one must consider that insiders could easily obtain financing to exploit an informational advantage (Dent 252). If insider trading were legal, insiders would be free to seek outside financing for trading. Insiders could borrow money for stock trading “on margin,” similarly to how outsiders do today (Dent 252). By having inside information and an almost guarantee of beating the market, they would be able to borrow more money than outsider investors. Lenders would have greater incentive to lend money to an insider rather than an outsider. Inside traders are less risky because returns are practically guaranteed. Due to this guarantee, insiders could also use more personal assets like their homes to secure loans that a prudent outsider would not or could not. This increased borrowing could multiply the trading capacity of insiders (Dent 252). Insiders could also sell their information. This would allow the wealthy to reap greater profits because they have greater capital to stake (Dent 252). Many question the fairness of widespread insider trading and the numerous unknown effects.

The 1920’s Argument

Some proponents defend against claims that IT will deter outside investment in the way that opponents speculate by making reference to the 1920’s stock market. Proponents say that insider trading was not clearly illegal in the 1920’s, yet did not deter outside trading (Dent 260). However, the stock market is different than it was in the 20’s. Most traders were individuals with little knowledge of risk. Nowadays, experienced firms and institutions do most of the trading. Also, no other foreign markets had barred insider trading yet, so there were not better alternatives than the U.S., markets in the 1920’s (Dent 260). If the U.S. legalized insider trading today, investors have the opportunity to simply invest in foreign markets instead. One should also note that the various conditions of the 1920’s market contributed to the Crash of 1929. Those who use this reference to historical conditions simply not consider the complexities of today’s markets. This paper will argue that IT could deter investments.

Unintended Consequences

As made evident by examining the two side of the ongoing debate, there are numerous potential flaws in the logic supporting the legalization of insider trading. There are also several potential unintended consequences that need to be considered by those forming their own opinion.

Managerial Conduct

Other than potentially causing employees to prevent a free-flow of information within the organization, legalizing insider trading could also have damaging effects on managerial conduct.

Permitting insider trading could drastically change decision-making by corporate executives. Insider trading may create greater incentives for executives and officers to make decisions that would increase the volatility of the company’s stock. There may be greater temptation to knowingly make risky or poor decisions in order to cause the company’s stock price to rise or fall because this would create the opportunity for insider trading (Dent 258). In such a circumstance, an executive could hypothetically manipulate the stock price in order to maximize his or her returns. For example, an officer may short sell the stock and then deliberately make poor decisions to cause the stock price to drop. Whilst this is an extreme case, one must think about the potential effects of legalized insider trading on human nature and the effects of greed on the human psyche when it is without consequences or penalties. Insider trading could be pervasive in managerial behavior.

Insider trading may also affect the disclosure of information. Executives would be faced with the choice of what information to release and when to release it. For example, consider a CEO who just received both good and bad news about the company. If he or she chooses to release both good and bad news at the same time, they would have a negated effect on the stock price. This would provide no opportunity for insider trading. In contrast, the CEO could first sell stocks and disclose bad news to the public, and then buy stocks and disclose the good news (Dent 257). The CEO would face the temptation to act in his or her selfish interest. In such a situation, outsiders ultimately lose as a result of the asymmetrical information, which wouldn’t have happened if the CEO released both pieces of information simultaneously.

Ultimately, legalizing insider trading creates incentives for a CEO or other executives to withhold information from peers and the board of directors. Executives may also be tempted to release false or misleading information in order to manipulate stock prices and receive profit, which violates federal securities laws (Dent 257). Conflicts in managerial decision-making, manipulation of the disclosure of information, and increase in the dissemination of false or misleading information are potential unintended consequences that could have significant negative effects on businesses, financial markets, and the economy.

As made evident by examining the two side of the ongoing debate, there are numerous potential flaws in the logic supporting the legalization of insider trading. There are also several potential unintended consequences that need to be considered by those forming their own opinion.

Managerial Conduct

Other than potentially causing employees to prevent a free-flow of information within the organization, legalizing insider trading could also have damaging effects on managerial conduct.

Permitting insider trading could drastically change decision-making by corporate executives. Insider trading may create greater incentives for executives and officers to make decisions that would increase the volatility of the company’s stock. There may be greater temptation to knowingly make risky or poor decisions in order to cause the company’s stock price to rise or fall because this would create the opportunity for insider trading (Dent 258). In such a circumstance, an executive could hypothetically manipulate the stock price in order to maximize his or her returns. For example, an officer may short sell the stock and then deliberately make poor decisions to cause the stock price to drop. Whilst this is an extreme case, one must think about the potential effects of legalized insider trading on human nature and the effects of greed on the human psyche when it is without consequences or penalties. Insider trading could be pervasive in managerial behavior.

Insider trading may also affect the disclosure of information. Executives would be faced with the choice of what information to release and when to release it. For example, consider a CEO who just received both good and bad news about the company. If he or she chooses to release both good and bad news at the same time, they would have a negated effect on the stock price. This would provide no opportunity for insider trading. In contrast, the CEO could first sell stocks and disclose bad news to the public, and then buy stocks and disclose the good news (Dent 257). The CEO would face the temptation to act in his or her selfish interest. In such a situation, outsiders ultimately lose as a result of the asymmetrical information, which wouldn’t have happened if the CEO released both pieces of information simultaneously.

Ultimately, legalizing insider trading creates incentives for a CEO or other executives to withhold information from peers and the board of directors. Executives may also be tempted to release false or misleading information in order to manipulate stock prices and receive profit, which violates federal securities laws (Dent 257). Conflicts in managerial decision-making, manipulation of the disclosure of information, and increase in the dissemination of false or misleading information are potential unintended consequences that could have significant negative effects on businesses, financial markets, and the economy.

Impairing the Functioning of Securities Markets

Perhaps the most important unintended consequence of legalizing insider trading is the potential to impair the functioning of securities markets (Dent 250). The SEC has said that "economic studies have provided support for the view that insider trading reduces liquidity, increases volatility, and may increase the cost of capital” (Dent 259). A few of these potential consequences have already been discussed, including increased cost of equity and increased volatility due to affected managerial conduct. The reduction of liquidity and the deterrent of investment are to be discussed in the following sections. It is pertinent to note that the SEC report regarding the potential ways insider trading impairs the efficient functioning of stock markets is based on the results of prohibited insider trading (Dent 259). If these results are seen even when IT is illegal, and therefore not significantly common, one must question the consequences of legalization.

Deterring Investment

As has been discussed, there are numerous ways that legalizing insider trading could deter outside investors from U.S. securities markets. First, disadvantaged outsider traders could be driven out of markets due to significant financing insiders could obtain. Second, investors could also choose to voluntary abandon U.S. markets and put money in foreign markets where IT is prohibited and they perceive it is fairer and less risky (Dent 260). There are also other factors that could contribute to deterring investment in U.S. markets.

Investors will invest in stocks if the securities market outperforms other available investments, which it currently does (Dent 262). If insider trading becomes rampant, however, trading for outsiders will no longer be the best investment in terms of risk and return. Public confidence in securities markets would suffer. Dent argues, “Not even the most sophisticated mutual fund could match the performance of even a minimally skilled insider. In such a world only a fool would utilize anything but an insider trading equity fund to trade stock” (262). In such a circumstance, the only people left trading are insiders. The obvious issue is that insiders can only trade if there are outsiders to trade with. Reduced public ownership of corporations and the number of overall traders in the market is a severe unintended consequence. The efficiency markets depends on a steady flow of trading.

Harm to Liquidity

Other than deterring outside investors, there could also be harm to markets’ liquidity. Deterring potential investors from equity markets ultimately makes those markets less liquid (Loss 34). Increased transactions costs and higher costs of equity reduce liquidity less investors are willing to trade in the market, which decreases cash flow (Matthews). Reduced liquidity means that intermediaries such as investment bankers will pay less for a company’s stock because they have to assume greater risk that they won’t be able to sell it when they want to. This makes the cost of raising capital more expensive for firms and it makes the economy less efficient overall (Matthews). Insider trading could make it incredibly difficult for a company to raise funds through means other owner equity.

Perhaps the most important unintended consequence of legalizing insider trading is the potential to impair the functioning of securities markets (Dent 250). The SEC has said that "economic studies have provided support for the view that insider trading reduces liquidity, increases volatility, and may increase the cost of capital” (Dent 259). A few of these potential consequences have already been discussed, including increased cost of equity and increased volatility due to affected managerial conduct. The reduction of liquidity and the deterrent of investment are to be discussed in the following sections. It is pertinent to note that the SEC report regarding the potential ways insider trading impairs the efficient functioning of stock markets is based on the results of prohibited insider trading (Dent 259). If these results are seen even when IT is illegal, and therefore not significantly common, one must question the consequences of legalization.

Deterring Investment

As has been discussed, there are numerous ways that legalizing insider trading could deter outside investors from U.S. securities markets. First, disadvantaged outsider traders could be driven out of markets due to significant financing insiders could obtain. Second, investors could also choose to voluntary abandon U.S. markets and put money in foreign markets where IT is prohibited and they perceive it is fairer and less risky (Dent 260). There are also other factors that could contribute to deterring investment in U.S. markets.

Investors will invest in stocks if the securities market outperforms other available investments, which it currently does (Dent 262). If insider trading becomes rampant, however, trading for outsiders will no longer be the best investment in terms of risk and return. Public confidence in securities markets would suffer. Dent argues, “Not even the most sophisticated mutual fund could match the performance of even a minimally skilled insider. In such a world only a fool would utilize anything but an insider trading equity fund to trade stock” (262). In such a circumstance, the only people left trading are insiders. The obvious issue is that insiders can only trade if there are outsiders to trade with. Reduced public ownership of corporations and the number of overall traders in the market is a severe unintended consequence. The efficiency markets depends on a steady flow of trading.

Harm to Liquidity

Other than deterring outside investors, there could also be harm to markets’ liquidity. Deterring potential investors from equity markets ultimately makes those markets less liquid (Loss 34). Increased transactions costs and higher costs of equity reduce liquidity less investors are willing to trade in the market, which decreases cash flow (Matthews). Reduced liquidity means that intermediaries such as investment bankers will pay less for a company’s stock because they have to assume greater risk that they won’t be able to sell it when they want to. This makes the cost of raising capital more expensive for firms and it makes the economy less efficient overall (Matthews). Insider trading could make it incredibly difficult for a company to raise funds through means other owner equity.

Market Failure

If corporations can no longer raise capital by selling securities, a major component of our financial system has been broken. Bhattacharya and Hazem argue that, in such a circumstance, corporations may be forced to pay stock exchanges a premium to limit insider trading (76). This would increase operating costs and decrease shareholder profits. This would be an unintended consequence because legalizing insider trading could lead to corporations attempting to prohibit it way other than legislation. Another possibility is that companies would then be forced to seek out investment from private equity companies, which often demand full control and do not tolerate insider trading (Dent 264). Dent argues that, ironically, insider trading could lead to the extinction of both securities markets and insider trading altogether (Dent 264). This would be the penultimate unintended consequence, and would obviously be counter-productive to what free-market enthusiasts are hoping to achieve by legalizing this practice.

Ultimately, there is a trade off involved in insider trading laws. Insider trading could increase market efficiency. Insider trading could also impact or eliminate U.S. securities markets, which would cause large firms would have to seek investment elsewhere (Dent 262). “A developed and modern securities market relies on the participation of different types of investors with different motivations and levels of expertise, and without insider trading laws many of these types of investors would stop participating” (Matthews). These are real potential costs that need to be analyzed and carefully weighed against potential benefits before drastic changes to long-standing regulations are made.

Alternate Suggestions

Several alternatives to current insider trading legislation have been proposed. One suggestion is that market professionals (securities analysts) should be allowed to trade on inside information (Goshen and Parchomovsky 1229). Researchers reason that these specialists “enjoy economies of scale and scope in processing firm-specific and external information” and are also removed from corporate decision-making (Stanislav). It is thought that allowing market professionals to trade on inside information could create more liquidity in securities markets and prevent the unintended consequences that have been discussed. (Stanislav). However, if market professionals could trade legally on private information, but insiders could not, public shareholders would still lose. Outside traders would still be at a disadvantage. There would still be harm caused.

Thomas Lambert proposed that corporations should be allowed to opt out of insider trading laws, only if insiders disclose their identities and the fact of their trading at the time of their trades (Dent 265). The main issue with this proposal is that anytime an insider traded, there would be massive speculation. An insider may trade because they need cash or have extra cash they want to invest. Insiders may not even be trading to exploit non-public information, but others will react to it. Outsiders will be unable to know why insiders are trading, so they can only guess and may often overreact. This would cause the stock’s price to be adjusted inefficiently (Dent 265). Dent argues that outsiders may attempt to protect themselves by only trading when insiders disclose information (Dent 265). This is another way that insider trading could disrupt the functioning of markets.

Lastly, John Carney also suggested there be an optional ban on insider trading rather than a mandatory one (Breslow). This is ultimately the same as legalizing the practice. It doesn’t force a company to permit or engage in the activity, but does not restrict it from doing so either. Breslow argues that under such a system, shareholders could discount shares to punish insider traders if IT created incentives that undermined executive performance or compromised managerial decision-making. This argument is based on the idea that a one-size-fits-all ban on insider trading is not the best available method in terms of maximizing benefits to market efficiency and minimizing unintended consequences.

The issue with the suggestion of optional insider trading is that it creates too many inconsistencies. It could put a company at odds with stockholders. It could also put the company’s board of directors and executives at odds with employees because they would be benefiting and reaping profit from knowledge and information generated by the employees’ work (Dent 267). The other concern with optional insider trading is how it should be monitored. It would be extremely difficult to regulate or to analyze. Investors would have to speculate on a case-by-case basis how pervasive insider trading was in each company. Those factors would also impair the functioning of securities markets and make them less efficient. It has proved to be challenging to identify changes to legislation that would not pose significant consequences.

If corporations can no longer raise capital by selling securities, a major component of our financial system has been broken. Bhattacharya and Hazem argue that, in such a circumstance, corporations may be forced to pay stock exchanges a premium to limit insider trading (76). This would increase operating costs and decrease shareholder profits. This would be an unintended consequence because legalizing insider trading could lead to corporations attempting to prohibit it way other than legislation. Another possibility is that companies would then be forced to seek out investment from private equity companies, which often demand full control and do not tolerate insider trading (Dent 264). Dent argues that, ironically, insider trading could lead to the extinction of both securities markets and insider trading altogether (Dent 264). This would be the penultimate unintended consequence, and would obviously be counter-productive to what free-market enthusiasts are hoping to achieve by legalizing this practice.

Ultimately, there is a trade off involved in insider trading laws. Insider trading could increase market efficiency. Insider trading could also impact or eliminate U.S. securities markets, which would cause large firms would have to seek investment elsewhere (Dent 262). “A developed and modern securities market relies on the participation of different types of investors with different motivations and levels of expertise, and without insider trading laws many of these types of investors would stop participating” (Matthews). These are real potential costs that need to be analyzed and carefully weighed against potential benefits before drastic changes to long-standing regulations are made.

Alternate Suggestions

Several alternatives to current insider trading legislation have been proposed. One suggestion is that market professionals (securities analysts) should be allowed to trade on inside information (Goshen and Parchomovsky 1229). Researchers reason that these specialists “enjoy economies of scale and scope in processing firm-specific and external information” and are also removed from corporate decision-making (Stanislav). It is thought that allowing market professionals to trade on inside information could create more liquidity in securities markets and prevent the unintended consequences that have been discussed. (Stanislav). However, if market professionals could trade legally on private information, but insiders could not, public shareholders would still lose. Outside traders would still be at a disadvantage. There would still be harm caused.

Thomas Lambert proposed that corporations should be allowed to opt out of insider trading laws, only if insiders disclose their identities and the fact of their trading at the time of their trades (Dent 265). The main issue with this proposal is that anytime an insider traded, there would be massive speculation. An insider may trade because they need cash or have extra cash they want to invest. Insiders may not even be trading to exploit non-public information, but others will react to it. Outsiders will be unable to know why insiders are trading, so they can only guess and may often overreact. This would cause the stock’s price to be adjusted inefficiently (Dent 265). Dent argues that outsiders may attempt to protect themselves by only trading when insiders disclose information (Dent 265). This is another way that insider trading could disrupt the functioning of markets.

Lastly, John Carney also suggested there be an optional ban on insider trading rather than a mandatory one (Breslow). This is ultimately the same as legalizing the practice. It doesn’t force a company to permit or engage in the activity, but does not restrict it from doing so either. Breslow argues that under such a system, shareholders could discount shares to punish insider traders if IT created incentives that undermined executive performance or compromised managerial decision-making. This argument is based on the idea that a one-size-fits-all ban on insider trading is not the best available method in terms of maximizing benefits to market efficiency and minimizing unintended consequences.

The issue with the suggestion of optional insider trading is that it creates too many inconsistencies. It could put a company at odds with stockholders. It could also put the company’s board of directors and executives at odds with employees because they would be benefiting and reaping profit from knowledge and information generated by the employees’ work (Dent 267). The other concern with optional insider trading is how it should be monitored. It would be extremely difficult to regulate or to analyze. Investors would have to speculate on a case-by-case basis how pervasive insider trading was in each company. Those factors would also impair the functioning of securities markets and make them less efficient. It has proved to be challenging to identify changes to legislation that would not pose significant consequences.

Excessive Penalties and Legislation

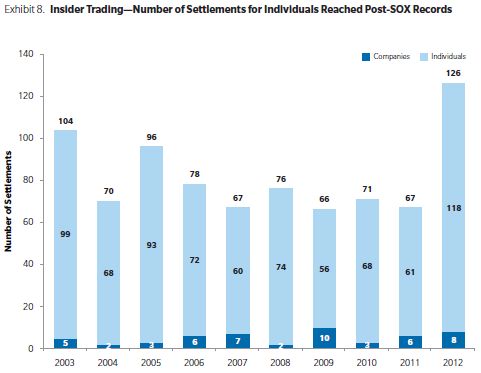

Economists and legal scholars do not agree on a desirable government policy toward insider trading. Thus, it is pertinent to address the current legislation because it is a serious point of contention among those deregulatory economists strongly in favor of legalization. Proponents say the punishment is too severe. The Insider Trading Sanctions of 1984 and Insider Trading and Securities Fraud Enforcement Act of 1988 increased the maximum criminal fine to $100,000 (Meulbroek 1664). Many believe the offense should be civil, not criminal, and that penalties should be more in line with the nature of the act. Deregulatory libertarians say the government is never justified in using intrusive enforcement measures developed to combat violent crime, like using a wire or tapping phones, for insider trading cases (Bandow). It is believed that the government’s strict enforcement may be discouraging even innocent information gathering done by specialists (Bandow). Proponents argue that the government should stop punishing investors seeking to act on the most accurate and timely information because that is what the financial markets should be about (Bandow). In consideration of these protests against harsh penalties, it is critical to note that the majority of insider-trading cases are in fact civil, rather than criminal. Seventy percent of defendants settle with SEC rather than go to court (Muelbroek 1664). The SEC usually seeks for the person to return profits gained or losses avoided, rather than go to jail or pay a fine.

The purpose of this paper is not to contest that IT laws are perfect, that aggressive criminalization of the act is cost effective, or that constant monitoring and surveillance of firms is economical. Perhaps there is room for the legislation to be updated, changed, or revised. However, there has to be more thought and consideration beyond simply legalizing it and seeing what happens. Despite what radical libertarians may believe, some regulation is necessary to a smooth-functioning financial system.

Conclusion

The global existence and enforcement of insider trading laws in stock markets is seen as a phenomenon of the 1990s. Before 1990, only thirty-four countries had laws prohibiting insider trading. Today, a study of one hundred and three countries that have stock markets reveals that insider-trading laws exist in eighty-seven of them (Bhattacharya and Hazem 75). Prohibiting IT has become more standard. The U.S. increased legislation in the 90’s due to the belief that insider trading was widespread in U.S. markets in the 1980’s. The United States is one of the only countries that strongly enforces insider trading legislation and prosecutes those who violate it.

Proponents often argue that insider trading is already so widespread that legalizing it would not have the negative effects that are speculated in this paper. This belief that insider trading is widespread rests on the assumption that insider trading significantly affects stock prices. To validate the belief that insider trading is widespread, proponents of insider trading often use empirical findings by Kewon and Pinkerton. These findings stated that, on average, forty to fifty percent of the price gain experienced by a target firm’s stock occurred before an actual take over announcement (Meulbroek 1662). Such research certainly depicts an asymmetry of information in the market. However, these figures do not allow one to confidently come to the conclusion that illegal insider trading is extensively pervasive in today’s securities market. Rather, it goes to show that some players, specifically market makers such as NASDAQ, possess superior information than individual or smaller investors. The employees of large investment banking firms and market makers go so far as to track the flights that corporate executives take in order to predict if there will be a merger or acquisition. The amount of time and money that goes into such information acquisition for speculation gives them an advantage. This asymmetry of information is not addressed in insider trading legislation, and is therefore not relevant as a point in case. In actuality, competition between informed insiders and informed outsiders, such as NASDAQ, can reduce the quality of the insider’s information (Lskavyan 208). Ultimately, Kewon and Pinkerton’s findings do not adequately justify the claim that insider trading is so widespread that any speculated consequences of legalization will be negligible. It is still largely unknown what the potential effects are.

Those in favor of legalization say insider trading is a victimless crime, but this is not entirely accurate. As long as outsiders are disadvantaged and made financially vulnerable, harm is inadvertently done. It is difficult to identify the specific victims of insider trading, similar to how it is difficult to single out victims of environmental pollution. In either case, harm is still caused (Dent 259). The potential adverse unintended consequences require a careful examination of what the true effects of legalization would be.

In a cross-country study done in 2005, Beny found that in countries with more prohibitive insider regulations, stock ownership is more diffused, prices are more accurate, and markets are more liquid (Dent 209). The work of numerous researchers referenced in this paper also supports these findings. Considering the numerous arguments this paper has outlined and the potential negative consequences that have been suggested, there is reasonable doubt about the true benefits of legalization. Considering the argument as it has been presented, it is hard to see how the reliance on the market to deter and sanction insider trading could be nearly as effective as the current (although admittedly imperfect) government regulation in place.

Economists and legal scholars do not agree on a desirable government policy toward insider trading. Thus, it is pertinent to address the current legislation because it is a serious point of contention among those deregulatory economists strongly in favor of legalization. Proponents say the punishment is too severe. The Insider Trading Sanctions of 1984 and Insider Trading and Securities Fraud Enforcement Act of 1988 increased the maximum criminal fine to $100,000 (Meulbroek 1664). Many believe the offense should be civil, not criminal, and that penalties should be more in line with the nature of the act. Deregulatory libertarians say the government is never justified in using intrusive enforcement measures developed to combat violent crime, like using a wire or tapping phones, for insider trading cases (Bandow). It is believed that the government’s strict enforcement may be discouraging even innocent information gathering done by specialists (Bandow). Proponents argue that the government should stop punishing investors seeking to act on the most accurate and timely information because that is what the financial markets should be about (Bandow). In consideration of these protests against harsh penalties, it is critical to note that the majority of insider-trading cases are in fact civil, rather than criminal. Seventy percent of defendants settle with SEC rather than go to court (Muelbroek 1664). The SEC usually seeks for the person to return profits gained or losses avoided, rather than go to jail or pay a fine.

The purpose of this paper is not to contest that IT laws are perfect, that aggressive criminalization of the act is cost effective, or that constant monitoring and surveillance of firms is economical. Perhaps there is room for the legislation to be updated, changed, or revised. However, there has to be more thought and consideration beyond simply legalizing it and seeing what happens. Despite what radical libertarians may believe, some regulation is necessary to a smooth-functioning financial system.

Conclusion

The global existence and enforcement of insider trading laws in stock markets is seen as a phenomenon of the 1990s. Before 1990, only thirty-four countries had laws prohibiting insider trading. Today, a study of one hundred and three countries that have stock markets reveals that insider-trading laws exist in eighty-seven of them (Bhattacharya and Hazem 75). Prohibiting IT has become more standard. The U.S. increased legislation in the 90’s due to the belief that insider trading was widespread in U.S. markets in the 1980’s. The United States is one of the only countries that strongly enforces insider trading legislation and prosecutes those who violate it.

Proponents often argue that insider trading is already so widespread that legalizing it would not have the negative effects that are speculated in this paper. This belief that insider trading is widespread rests on the assumption that insider trading significantly affects stock prices. To validate the belief that insider trading is widespread, proponents of insider trading often use empirical findings by Kewon and Pinkerton. These findings stated that, on average, forty to fifty percent of the price gain experienced by a target firm’s stock occurred before an actual take over announcement (Meulbroek 1662). Such research certainly depicts an asymmetry of information in the market. However, these figures do not allow one to confidently come to the conclusion that illegal insider trading is extensively pervasive in today’s securities market. Rather, it goes to show that some players, specifically market makers such as NASDAQ, possess superior information than individual or smaller investors. The employees of large investment banking firms and market makers go so far as to track the flights that corporate executives take in order to predict if there will be a merger or acquisition. The amount of time and money that goes into such information acquisition for speculation gives them an advantage. This asymmetry of information is not addressed in insider trading legislation, and is therefore not relevant as a point in case. In actuality, competition between informed insiders and informed outsiders, such as NASDAQ, can reduce the quality of the insider’s information (Lskavyan 208). Ultimately, Kewon and Pinkerton’s findings do not adequately justify the claim that insider trading is so widespread that any speculated consequences of legalization will be negligible. It is still largely unknown what the potential effects are.

Those in favor of legalization say insider trading is a victimless crime, but this is not entirely accurate. As long as outsiders are disadvantaged and made financially vulnerable, harm is inadvertently done. It is difficult to identify the specific victims of insider trading, similar to how it is difficult to single out victims of environmental pollution. In either case, harm is still caused (Dent 259). The potential adverse unintended consequences require a careful examination of what the true effects of legalization would be.

In a cross-country study done in 2005, Beny found that in countries with more prohibitive insider regulations, stock ownership is more diffused, prices are more accurate, and markets are more liquid (Dent 209). The work of numerous researchers referenced in this paper also supports these findings. Considering the numerous arguments this paper has outlined and the potential negative consequences that have been suggested, there is reasonable doubt about the true benefits of legalization. Considering the argument as it has been presented, it is hard to see how the reliance on the market to deter and sanction insider trading could be nearly as effective as the current (although admittedly imperfect) government regulation in place.

RSS Feed

RSS Feed