If you were to ask the average person on the street what was the cause of the great depression, nine out ten would say the stock market crash; the 10th would say, “What depression”. However most economists would agree, that the stock market crash would have led to a severe recession and it was actually the actions of the well-intentioned Federal Reserve Bank that turned the recession into a depression.

Up until that time, the 1920’s was unlike any other decade in the history of the United States. The newly formed Federal Reserve Bank was exerting some form of stability on the more than 25,000 banks in the United States, and because of technology, the car and housing industry were expanding (many homes were getting both electrified and internal plumbing) and the stock market was booming, in part because of buying on the margin. We were also on the gold standard. In other words, even though there was an abundance of paper money, many of these, gold certificates, could be redeemed for gold, generally $1-$50 gold pieces.

When buying a stock on the margin, your stockbroker lends you money, and then charges you interest plus the commission on the sale. During the 1920’s, the margin rate was 90% (it’s currently 50% and is determined by the FED). In other words, you would be able to buy $1000 worth of stock while only putting up $100. For instance, if you want to buy 100 shares of General Electric (the only stock that has been on the Dow Jones Industrial Average since its inception in 1896), that was selling for $10, you would give your broker $100 and he would lend you the other $900. In an up market, this is great. If the stock increases to $15 and you sell, you pay your broker back and receive $500 on your $100 investment (less interest and commissions). But what happens if the stock decreases to $5? The broker has what’s known as a margin call. Essentially, he wants his money. At that time everyone was in the market because of the high margin rate including blue collar workers. These people didn’t have the money, so they are out there $100, the broker is out their money, and since many brokerage houses were banks or borrowed from banks, the banks were out their money. At the time there was no FDIC and your money in the bank wasn’t insured. As a result, it wasn’t long before word got out and there was then an immediate run on the banks.

Up until that time, the 1920’s was unlike any other decade in the history of the United States. The newly formed Federal Reserve Bank was exerting some form of stability on the more than 25,000 banks in the United States, and because of technology, the car and housing industry were expanding (many homes were getting both electrified and internal plumbing) and the stock market was booming, in part because of buying on the margin. We were also on the gold standard. In other words, even though there was an abundance of paper money, many of these, gold certificates, could be redeemed for gold, generally $1-$50 gold pieces.

When buying a stock on the margin, your stockbroker lends you money, and then charges you interest plus the commission on the sale. During the 1920’s, the margin rate was 90% (it’s currently 50% and is determined by the FED). In other words, you would be able to buy $1000 worth of stock while only putting up $100. For instance, if you want to buy 100 shares of General Electric (the only stock that has been on the Dow Jones Industrial Average since its inception in 1896), that was selling for $10, you would give your broker $100 and he would lend you the other $900. In an up market, this is great. If the stock increases to $15 and you sell, you pay your broker back and receive $500 on your $100 investment (less interest and commissions). But what happens if the stock decreases to $5? The broker has what’s known as a margin call. Essentially, he wants his money. At that time everyone was in the market because of the high margin rate including blue collar workers. These people didn’t have the money, so they are out there $100, the broker is out their money, and since many brokerage houses were banks or borrowed from banks, the banks were out their money. At the time there was no FDIC and your money in the bank wasn’t insured. As a result, it wasn’t long before word got out and there was then an immediate run on the banks.

In times of economic and/or geopolitical strife, there is a “flight to hard assets”, specifically gold; and that’s exactly what was happening. People were trading in their paper money for gold and the United States treasury didn’t have enough gold to meet its obligations. The Secretary of the Treasury at the time was Andrew Mellon was also the Treasury Secretary under Coolidge and Harding prior to Hoover. Mellon was highly respected. Also, economics was in its infancy. The prevailing school of thought was classical (think Adam Smith, David Ricardo) and economists at the time felt the government should have no role in economics and the economy was self-correcting; therefore, when Hoover asked his advisors what we should be doing, the response from economists, including Irving Fisher (one of the foremost economists of the time) was to do nothing, government intervention will only make it worse.

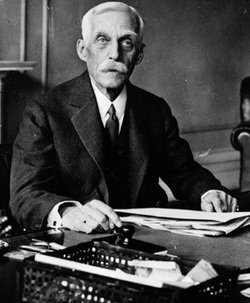

The run on gold reserves was a major problem and something had to be done. Mellon(pictured at left) had an idea. He went to the chairman of the FED, Eugene Meyer and shared his idea. What Mellon wanted the FED to do was shrink the money supply. His logic was that if there isn’t that much paper currency to circulate, economic entities wouldn’t be able to drain the Treasury’s gold reserve. Eugene Meyer was concerned that this lack of liquidity would cause a number of banks to fail. Mellon’s response was that this would be good for the economy; “it would weed out the weak banks. Meyer reluctantly agreed and between 1929 and 1933, the money supply contracted from $26 billion to $19 billion (a more advanced analysis will show that the currency to deposit ratio increased as did the reserve to deposit ratio which significantly lowered the money multiplier). As a result, it certainly did weed out the weak banks. Between 1929 and 1933, 9000 banks failed, 4000 alone in 1933. The worst year of the depression was 1933 with an unemployment rate of 25%, the real unemployment rate (which includes marginally attached and part time workers) was estimated at 50%.

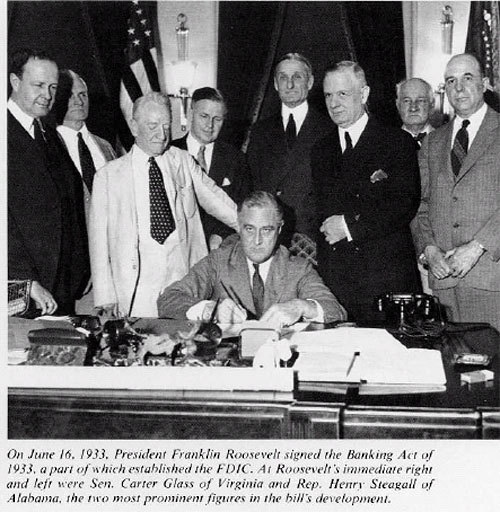

In March of 1933, FDR took office and instituted a number of reforms. Most notably was the Glass-Steagall act, which separated the function of Investment banking from consumer/business banking. This also established the FDIC which beginning 1-1-34, insured deposits up to $2000. Later that year it was increased to $5000. The Gold Reserve Act was also passed that pegged the price of gold at $35 ounce and made it illegal for individuals to own gold. Our money was now fiat money. Fiat money is money because the government states that it is money but more importantly, it is money because it is accepted as money by the populace and international trading partners.

Glass-Steagall and the FDIC restored immediate confidence in the banking system, and as a result, there were less than 65 bank failures in 1934. For the rest of the decade, the economy made a slow recovery and by 1941, the unemployment rate was 10.1%. However, within 2 years the unemployment rate was down to 1.7% as a result of the government spending vast amounts of money (48% of GDP) as a result of WW II.

Two afterthoughts:

In 1932, Congress began impeachment proceedings of Andrew Mellon; however he resigned and was given an Ambassadorship position.

There are times when we do learn from history. During the financial crisis of 2008 and subsequent recession, then FED Chairman Ben Bernanke (a true scholar of the depression), injected huge amounts of liquidity into the banking system greatly increasing reserves and the FED balance sheet which increased from $800 billion to over $4 trillion, thus avoiding what could conceivably have been a 2nd depression in 100 years. I firmly believe that history will be very kind to Chairman Bernanke.

Glass-Steagall and the FDIC restored immediate confidence in the banking system, and as a result, there were less than 65 bank failures in 1934. For the rest of the decade, the economy made a slow recovery and by 1941, the unemployment rate was 10.1%. However, within 2 years the unemployment rate was down to 1.7% as a result of the government spending vast amounts of money (48% of GDP) as a result of WW II.

Two afterthoughts:

In 1932, Congress began impeachment proceedings of Andrew Mellon; however he resigned and was given an Ambassadorship position.

There are times when we do learn from history. During the financial crisis of 2008 and subsequent recession, then FED Chairman Ben Bernanke (a true scholar of the depression), injected huge amounts of liquidity into the banking system greatly increasing reserves and the FED balance sheet which increased from $800 billion to over $4 trillion, thus avoiding what could conceivably have been a 2nd depression in 100 years. I firmly believe that history will be very kind to Chairman Bernanke.

RSS Feed

RSS Feed